Over the past years, interest rates have plummeted to historically low rates. This has resulted in yield-starved commercial real estate investors taking cover in alternative investments like Real Estate Investment Trusts (REITs).

As REITs offer stable revenues, value-adding, and traceability of assets, investors deem them low-risk investments. But, with interest rates likely to soar shortly, many investors are concerned about the impact of the rising interest rates on the REITs and commercial real estate property values and performance.

It is commonly perceived that rising interest rates may cause capitalization rates to increase and property values to fall. Hence, rising interest rates will result in weaker overall returns on investment.

However, interestingly, historical records suggest that rising interest rates are not necessarily correlated with REIT performance. Contrary to popular belief, REITs are among the most profitable investments to make in a rising interest rate environment. Let’s discuss why.

Rising interest rates vs REIT returns

Many investors assume that as a rule of thumb, rising interest rates are inimical to REIT returns. They believe that rising interest rates are inversely proportional to REIT returns and performance. However, this is a misconception.

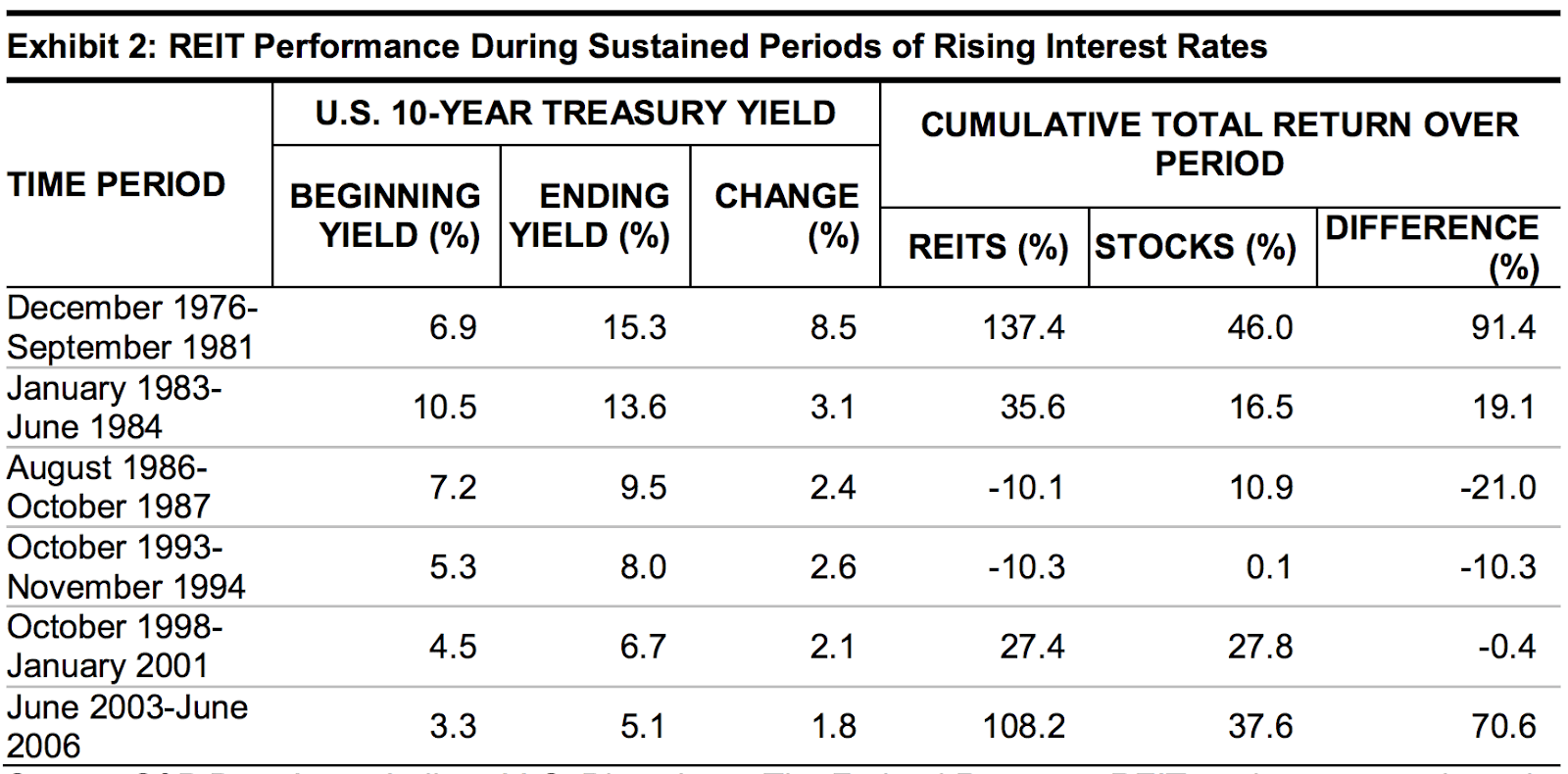

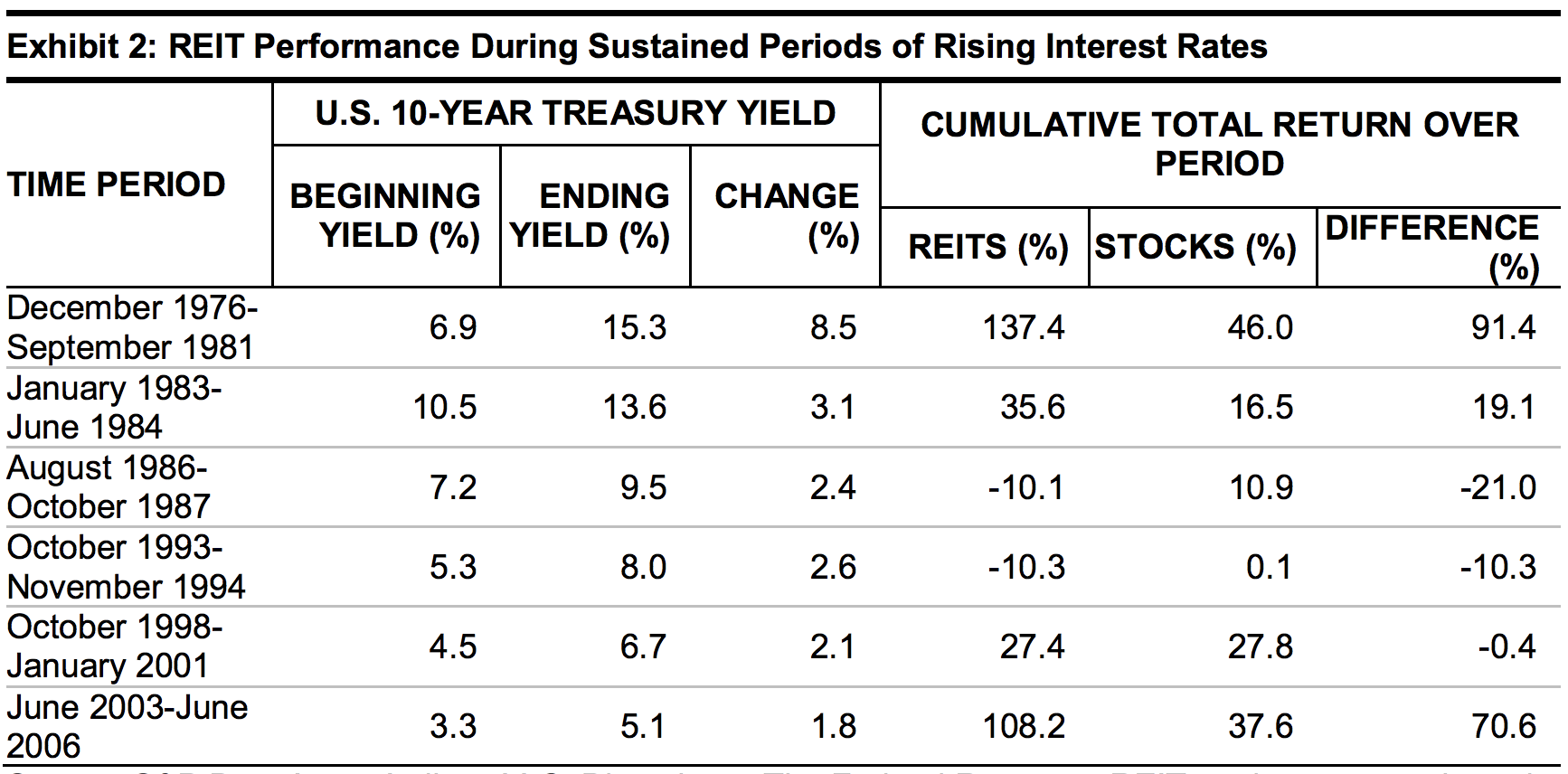

Standard and Poor (S&P) analyzed six periods beginning in the 1970s. During this period, the yield of the 10-year treasury grew substantially. The study compared the rising interest rates during that period to the performance of the REITs and stock bonds.

{kind=link}

It is observed that of the six periods of rising interest rates, four periods recorded increased REIT returns. Furthermore, in half of those periods, the REITs outperformed S&P 500.

Moreover, The National Council of Real Estate Investment Fiduciaries (NCREIF) observes that in the period between 1996 and 2017, rising interest rates affected over 19 quarters. In this case, also, listed equity REITs secured consistent positive returns.

Why do REITs react positively to rising interest rates?

Several factors determine the overall returns of the REITs depending on a specific interest-rate climate. Firstly, REITs operate in diverse asset classes. In commercial real estate, REITs invest in diverse models ranging from multifamily, industrial, office, retail, hospitality, and so on. This means that each of these properties is positioned across various sectors.

Hence, indisputably, each of these property types will have individual, unique variables that will react differently to the changing dynamics of the interest environment.

Besides, rising interest rates indicate economic growth and inflation. Both of these factors translate into increased demand for real estate. This in turn impacts REIT positively.

Since the economy is recovering, it allows REITs to acquire new properties and expand their asset base. As a result, healthy economic growth boosts REIT earnings dividend and cash flow. In addition to this, during inflationary periods commercial real estate owners enjoy higher occupancy. They can also increase rents thereby generating more cash flow and contributing to the REIT’s dividend growth.

In the property types where the leases are of shorter periods like multifamily, hotels, and self-storage, the landlords renew leases more frequently unlike the properties with long-term leases.

Hence commercial real estate owners can leverage contractual rent increases and positive lease renewals to offset some of the impacts of rising interest rates.

Therefore, it is evident that REITs have historically exhibited resilience and a positive association with inflation.

However, commercial real estate landlords exercise the ability to raise the rent in an improving economy to keep up with rising interest rates. Hence higher rents also add value to the properties and strengthen their potential.

Rising interest rates vs REIT debt exposure

To avoid paying corporate taxes REITs distribute 90% of their taxable income to the shareholders as unqualified dividends. therefore they obtain Finance for their business in the form of external debts and equity capital from investors.

As a result, higher interest rates increase the REIT’s cost of debt. Furthermore, this can impact its profit margins and FFO. However, many REITs carry a fixed rate of debt.

Most of the REITs have drawn out the average maturity period of their debt to 75 months. Hence, REITs have locked in the low-interest rates well until the next decade. Therefore, a rise in the interest rates will affect the REITs less than anticipated.

Asset management and new acquisitions of properties

A rise in the interest rates will increase the real estate capitalization rates. This stimulates the REITs to further invest in new assets. REITs take on more debt at higher interests to secure financing for constructing or acquiring new projects like multifamily, industrial, office, and so on.

However, obtaining debt at higher interest rates increases borrowing costs and decreases the returns for the REITs.

In such cases of overbuilding amidst rising interests, REITs must seek to employ skilled property and asset managers. This is because these professionals have the expertise to increase cash flow per unit by utilizing factors that are independent of interest rate dynamics.

For instance, property managers can refurbish the property units with high-quality newer appliances that are purchased at huge discounts.

Moreover, with unsecured debt issuances in the capital markets and lowering property taxes from assessment appeals asset managers can secure higher rents or diminish the overall expenses of a property or a portfolio.

Hence the REITs can continue to yield lucrative returns and meaningful value creation even during a high-interest rates environment.

Furthermore, REITs only use a limited amount of debt. As a result, the positive outcomes of a strong economy surpass the adverse impacts of higher interest rates.

Short-term interest rate changes

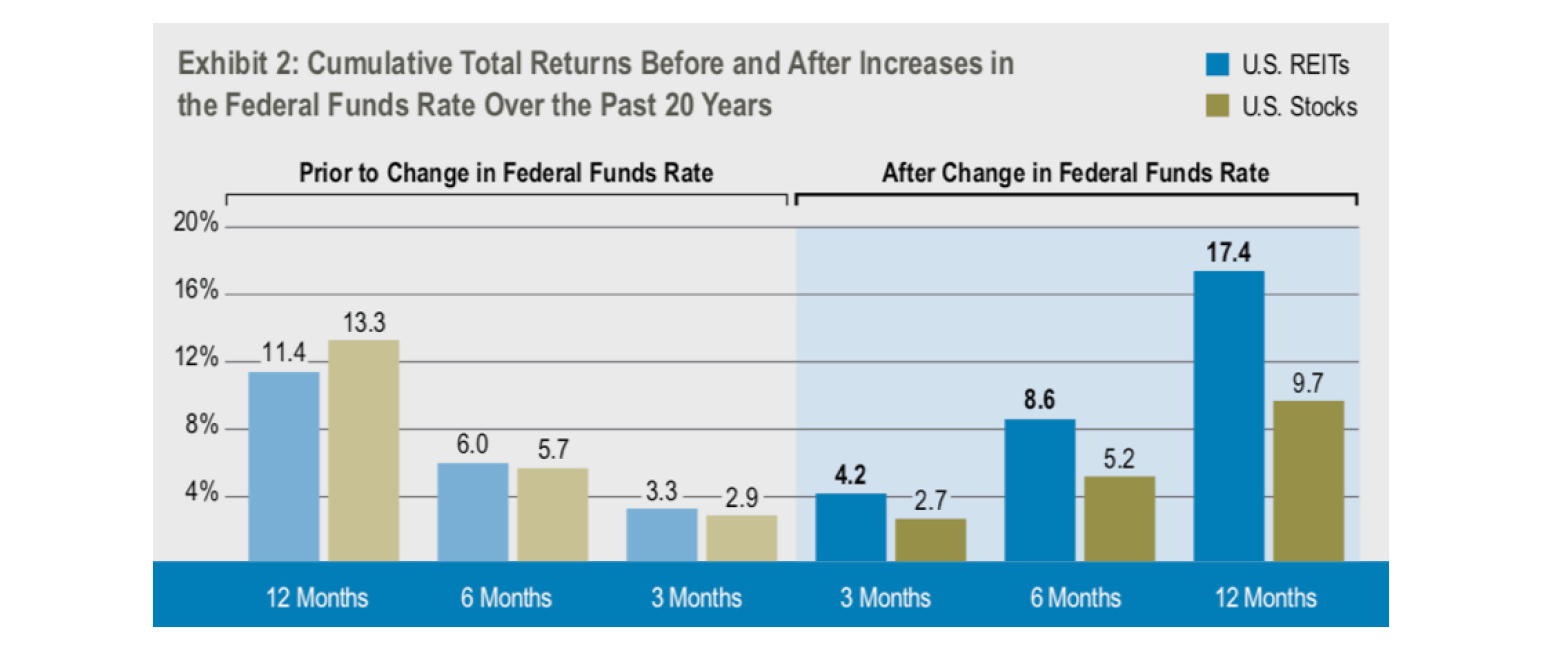

According to Cohen & Steers, the underperformance of REITs generally tend to last for relatively shorter terms. This correlates directly to The Federal Reserve’s decision to hike interest rates due to a bolstering economy. Due to consecutive quarters of high GDP and low unemployment, the Fed may increase the rates which result in the REIT shares moving in the direction of interest rates.

However, the decline in the REIT’s performance is brief and spread over a short period. Cohen&Steers observe that over 20 years, in the three months after a hike in the Federal interest rates, the U.S. REITs outplayed the stocks by a meager 1.5%. Over the next 12 months, the REITs returned to 17.4% on average outperforming the stocks by 7.7%.

Real estate REITs will benefit from a rising interest rate environment

After a careful analysis of historical data on the correlation between REITs and interest rates, it is clear that fluctuations in interest rates are certainly not the key drivers of REITs in the medium or long term. Although, REIT returns and values are not fixed and can vary during different interest rate environments, majorly, REITs react positively to rising interest rates.

This is because REITs are equipped with experienced management teams who can uncover strong value and dividends even amidst inflation.

They can increase rents or add income-generating services to the commercial properties or expand the REIT’s asset base to ensure that the commercial real estate investors can continue to receive higher dividends on their shares.

Therefore, if interest rates rise gradually, strong REIT fundamentals can easily overshadow the negative impacts of the rising interest rates.